Understanding credit data can be challenging for beginners, as it combines numbers, scores, accounts, and payment histories. Understanding how to read and interpret this data is important for individuals, students, and businesses in order to make wiser financial choices. This has been simplified today by credit report generators. These online generators enable the arrangement of credit data in a standard and simple form, as opposed to handling the complex reports manually.

This guide will cover how to use credit data through credit report generators, what to interpret in a credit report, and how to use the information profiled in a credit report.

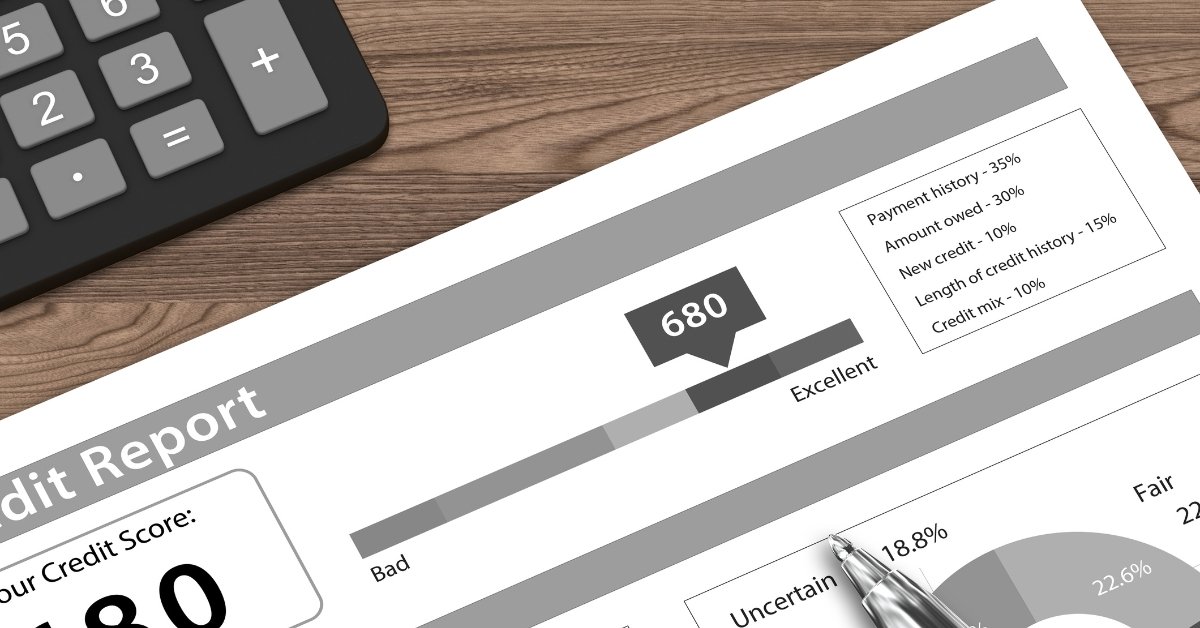

What Is Credit Data?

Credit information embodies a depiction of your financial conduct in the long-term. It encompasses your borrowing patterns, your repaying patterns, and how much you use credit.

There are various types of information presented in a typical credit report that outline a whole financial picture.

| Data Type | Description | Example |

| Personal Info | Identity details | Name, address |

| Credit Accounts | Loans and cards | Credit card, personal loan |

| Payment History | Record of payments | On-time or late payments |

| Credit Limits | Maximum allowed credit | $10,000 limit |

| Credit Usage | Amount used | $3,000 used |

| Inquiries | Credit checks | Loan application |

Understanding these components is the first step toward proper analysis.

What Is a Credit Report Generator?

A credit report generator is an application that systematizes credit-related information into a structured report format. It assists the users to see, manage, and interpret financial data in an easier way.

Some of the common uses of a credit report maker include:

- Understanding credit report mechanisms.

- Making practice in financial analysis.

- Assessment of financial behavior.

- Arranging sample or actual credit information.

Generators make the process simpler as opposed to the manual creation of reports, which minimizes errors.

Key Components to Analyze in a Credit Report

To effectively interpret credit data, it is necessary to divide the report into systematic blocks and interpret the meaning of each of them. All the components give different information about financial behavior, and a combination of all the components will give a complete credit profile.

1. Personal Information Section

The personal information section holds the identity details, including name, address, and identification data. Though it might appear to be elementary, it is the core of the whole report.

| Element | What to Check |

| Name & Identity | Correct spelling and format |

| Address | Current and previous addresses |

| Identification Data | ID numbers or linked details |

The slightest mistake in this section may cause misunderstandings or wrong reporting. This is one of the parts that must always be checked prior to the analysis of financial data.

2. Credit Accounts (Tradelines)

Here you will find a list of all your credit accounts, including those that are closed and those that are active.

Key things to analyze:

- Number of accounts

- Form of credits (credit cards, loans, etc.)

- Status of account (open, closed, overdue)

- Credit limits vs balances

What to look for:

- Excessive open accounts can be a sign of excessive reliance on credit.

- Accounts that are managed well exhibit responsible use.

3. Payment History

One of the most significant components of credit information is payment history, since it shows stability.

Things to analyze:

- Number of on-time payments

- Frequency of late payments

- Any missed payments

Example:

- Timely payments – Good financial discipline.

- Delay frequent -Potential risk indication.

Even several late payments may influence the overall analysis.

4. Credit Utilization Ratio

Credit utilization is used to gauge the extent of the usage of your credit. It is a major indicator of financial strength.

| Credit Limit | Used Amount | Utilization | Interpretation |

| $10,000 | $2,000 | 20% | Healthy usage |

| $10,000 | $4,000 | 40% | Moderate usage |

| $10,000 | $8,000 | 80% | High risk |

Formula:

Credit Utilization = (Used Credit ÷ Total Limit) × 100

The decreased use implies more control, and increased use can imply financial stress.

5. Credit Inquiries

The section records the frequency with which your credit has been used.

Types of inquiries:

- Soft inquiries (no impact)

- These are hard inquiries (associated with credit applications).

What to analyze:

- Excessive questions within a limited duration can spell financial pressure.

- It is not unusual to ask questions occasionally.

6. Public Records and Additional Data

A few credit reports contain financial or legal histories that give more details concerning the financial behavior.

Why it matters:

- These records can show severe financial incidents.

- They may have a substantial effect on general credit analysis.

- It should be precise since errors in this part are misleading.

This part must take time before it is checked again to certify that all the information is right and updated.

Read our Blog on “5 Reasons to Create a Credit Report Before Applying for Loan”

Step-by-Step Process to Analyze Credit Data Using Generators

To get meaningful insights, follow a structured analysis process.

Step 1: Input Accurate Data

Start by entering complete and correct data into the generator. If the data is incorrect, the analysis will also be inaccurate.

Step 2: Generate the Structured Report

Organize your data into sections like accounts, payments, and balances. This structured format makes it easier to analyze.

Step 3: Break Down Each Section

Instead of reviewing the report as a whole, analyze each section separately:

- Personal details

- Accounts

- Payments

- Balances

This helps avoid confusion.

Step 4: Identify Patterns in Data

Look for repeating trends such as:

- Consistent payment behavior

- Increasing or decreasing balances

- Frequent credit usage

Patterns give more insight than single data points.

Step 5: Compare Reports Over Time

If you have multiple reports, compare them to track changes:

- Has your credit usage improved?

- Are payments becoming more consistent?

- Are balances decreasing?

This shows progress or decline.

Step 6: Draw Practical Conclusions

After analysis, summarize your findings:

- Strengths (e.g., consistent payments)

- Weaknesses (e.g., high utilization)

- Areas to improve

This step turns data into actionable insight.

Advanced Tips for Better Credit Data Analysis

To analyze credit data properly, it is necessary to go beyond the numbers and see the general patterns and behavior.

-

Focus on Trends, Not Just Numbers

Single numbers do not provide the whole picture. Analyze the change of your data with time rather than looking at one value. Trends enable you to know whether you are getting better or worse in your financial situation.

-

Combine Multiple Data Points

Always analyze data as a team and not individually. As an illustration, the combination of a high credit usage and late payments is a better alarm compared to either of the two factors. Integrating data is more informative.

-

Avoid Overanalyzing Small Changes

Minor changes in balances or utilization are usual. Actually, you should listen to long-term behavior and patterns rather than minor changes.

-

Use Data for Planning

The credit information must get you into action. Your analysis can be used to understand how to better spend, credit, and how to better plan finances.

Final Thoughts

Using credit data is an effective means of working out the financial behavior and decision-making. Although the data might appear complicated to some users, the credit report maker makes it easier by structuring the whole information into a systematic format.

Consistency is the key to an effective analysis. Considering your credit information on a regular basis, examining trends and acting upon them can also lead you to better financial habits over time.

Credit data will be much more than information; once the correct approach is taken, it will be a means of smarter financial control and long-term stability.

FAQs

What is the purpose of analyzing credit data?

Credit data analysis enables you to know your financial dynamics, detect risks, and make a good choice to enhance credit health and general financial management.

Are credit report generators reliable for analysis?

Yes. The credit report generators can arrange the complicated data into a format that is easy to read, and analysis is quicker, more precise, and less likely to suffer from human factors.

How often should I analyze my credit data?

Credit information should be checked regularly, i.e., monthly or quarterly. The regular monitoring assists in monitoring the progress and uncovering problems early.